1. Upcoming Tax Reform in Indonesia

The tax reform announced in May 2024 introduces significant changes to the Indonesian tax

system. Two key updates include the integration of the National ID Number (National ID) as

the Taxpayer Identification Number (TIN) and the implementation of the Core Tax

Administration System (CTAS).

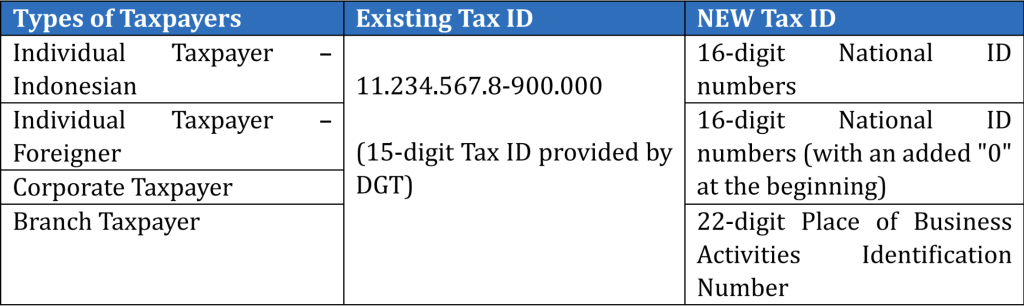

1.1 Integration of National ID into TIN:

Starting from July 1, 2024, the National ID will serve as the TIN for taxpayers. This integration aims to synchronize, verify, and validate taxpayer data, streamlining registration and data management processes. The Directorate General of Taxes (DGT) will have access to

both financial and non-financial data of taxpayers, enhancing tax collection and supervision efficiency

Taxpayer Registration

Individuals who already possess a National ID will need to fulfill subjective and objective obligations and apply for taxpayer registration to obtain a TIN. The DGT will then activate their National ID as the TIN.

Grace Period

Taxpayers who have not yet matched their National ID as their TIN have until July 1, 2024, to do so. Failure to comply will result in the inability to access tax and administrative services provided by other parties.

Taxpayer Support

The DGT encourages taxpayers to match their National ID data as their TIN and prepare their information systems accordingly for the implementation of the new TIN format and Place of Business Activities Identification Number.

1.2 Implementation of the Core Tax Administration System (CTAS)

The CTAS is a redesigned tax administration system that improves the DGT’s core system limitations. It utilizes a Commercial Off-the-Shelf (COTS)-based information system and enhances the tax database for easy, reliable, integrated, accurate, and definite tax processes.

Benefits of CTAS implementation include availability of taxpayer accounts on the DGT portal, improved service quality, reduced potential for tax disputes, and changes in business processes.

The CTAS implementation will bring changes to the DGT’s business processes, integrating various core functions and focusing on digital services. This includes 21 amended business processes related to registration, tax return management, payment, taxpayer account

management, data processing, exchange of information, compliance risk management, and more.

Currently, the CTAS is on testing stage by the DGT and will be announced by the DGT on its release and implementation in the next half of 2024.

2. DGT Releases Circular Letter on Implementation of Tax Obligations in Bonded Zones

On 20th May 2024, the DGT releases a Circular Letter No. SE-3/PJ/2024 concerning Elucidation on the Implementation of Tax Obligation in Bonded Zone (“SE-3/2024”).

This circular letter stipulates that the provision of Bonded Zone facilities aims to encourage exports which are a national priority at Bonded Stockpiling Area (TPBs).

SE-3/2024 provides elucidation on the following matters:

(a) Entry of Taxable Goods (BKPs) into Bonded Zone:

BKPs can be brought into the Bonded Zone through import or delivery from specified zones or places within the customs area. Tax in the Context of Import is not collected on the import of BKPs. When BKPs are delivered from specified zones, Value Added Tax (PPN) or PPN and Sales Tax on Luxury Goods (PPnBM) are not collected. Similarly, when BKPs are delivered by Taxable Entrepreneurs (PKPs) to Bonded Zone Entrepreneurs, Operators, or PDKBs from other places within the customs area, PPN or PPN and PPnBM are not collected.

(b) Requirements for Non-Collection of PPN or PPN and PPnBM

To qualify for the non-collection of PPN or PPN and PPnBM for the delivery of BKPs into the Bonded Zone, Bonded Zone entities must have an approval document for the entry of goods into the Bonded Zone before preparing the Tax Invoice. Additionally, if there is a receipt of payment before the delivery of BKPs, the approval document must be obtained before preparing the Tax Invoice, including the Tax Invoice for the receipt of payment.

(c) Release of BKPs from Bonded Zone

BKPs owned by Bonded Zone entities can be released from the Bonded Zone for export purposes, delivery to other specified zones, or delivery to other places within the customs area. The release of BKPs for export purposes is subject to PPN at a rate of 0%. Delivery of BKPs to other specified zones is subject to PPN or PPN and PPnBM according to the taxation facilities applicable in the destination area. Delivery of BKPs to other places within the customs area is subject to PPN or PPN and PPnBM.

(d) Release of BKPs owned by foreign tax subjects from Bonded Zone

BKPs owned by foreign tax subjects can be released from the Bonded Zone for export, delivery to other specified zones, or delivery to other places within the customs area. Exports of BKPs are not subject to PPN. Delivery of BKPs to other specified zones is not subject to PPN if the foreign tax subject conducting the delivery does not have a permanent establishment as a PKP. However, the delivery of BKPs to another place within the customs area is subject to PPN or PPN and PPnBM.

3. Indonesia’s Import Quota Policy Faces Challenges and Revisions

The Indonesian government’s implementation of import quotas through Ministry of Trade (MOT) Regulation No. 36 of 2023 has generated objections and concerns from various stakeholders. Critics argue that these quotas could disrupt the supply chain and availability of goods in the domestic market. In response to feedback, the government has made revisions, with the most recent being MOT Regulation No. 8 of 2024, effective from May 17, 2024.

Import quotas are non-tariff trade barriers set by the government to limit the quantity of specific goods that can be imported into the country within a certain period. The Ministry of Trade regulates these quotas, requiring importers to obtain an Import Approval (PI) as part of their Business Licensing in the import sector.

The PI outlines the quota of products that can be imported by a company, specifying the goods’ classification, quantity, and country of origin, among other details. The Ministry of Trade considers Commodity Balance and Technical Considerations from relevant ministries to determine the import quota for specific product categories.

However, the implementation of these import quotas has presented challenges for importers. The backlog of containers at major Indonesian ports due to slow issuance of PI and Technical Considerations has caused operational instability and delays. Importers have also faced additional compliance costs and limitations on their import quotas, which may reduce the availability of imported products in the domestic market.

To address these issues, the government has revised MOT Regulation 36 by issuing MOT Regulation No. 8 of 2024. The new regulation provides relaxation on import licensing for certain commodities, such as traditional medicine, health supplements, cosmetics, household supplies, bags, valves, electronics, footwear, apparel, and accessories. The president has also directed relevant ministries to expedite the issuance of PI and completion of Technical Considerations to accelerate the settlement of import licensing issues.

While the relaxation of import licensing is positive news for businesses, it is important to remain vigilant due to the dynamic nature of the Ministry of Trade’s regulations. Future changes and adjustments to the import quota policy may still occur.

This Client Alert is intended for informational purposes only and does not constitute legal or formal tax advice. Any reliance on the material contained herein is at the user’s own risk. You should contact a consultant in your jurisdiction if you require legal advice.